- We are raising our target price for Astor Enerji from TRY 324.90, set on January 23, 2026, to TRY 403.50, reflecting our updated assumptions and revised outlook. We maintain our "Outperform" rating on the stock. Consistent with our previous report, we continue to employ a Discounted Cash Flow (DCF) methodology in our valuation. Our new target price implies an upside potential of approximately 96% from the current share price.

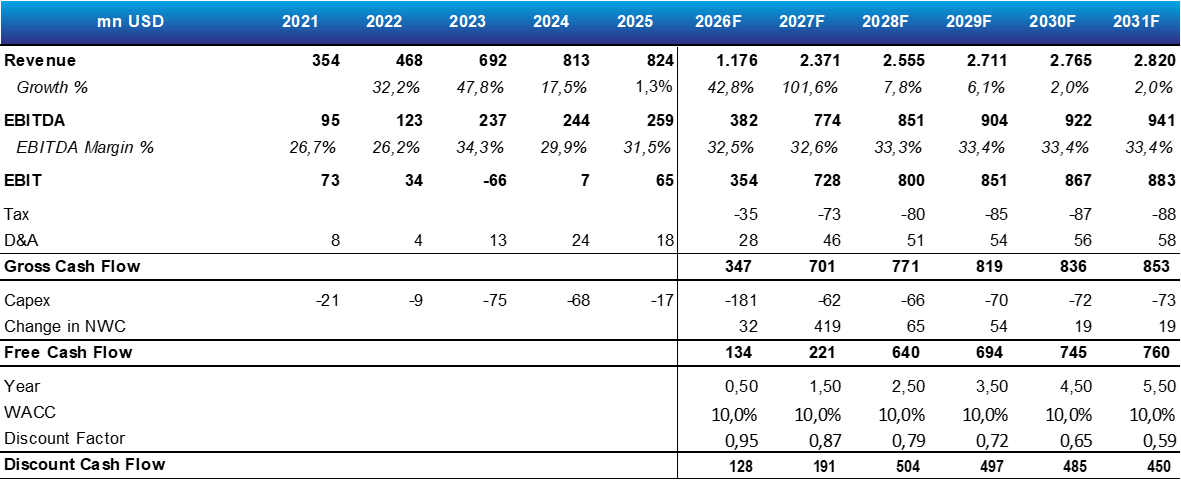

- New orders drive capacity utilization assumptions higher… The company's newly announced commercial agreement totaling $768.9mn - equivalent to approximately 96% of its 2025 revenues - signals robust demand for newly commissioned capacities. Accordingly, we are revising our capacity utilization rate (CUR) assumptions upward for the new facilities; we raise our CUR estimate for the second plant from 51% to 70%, and for the third plant from 45% to 70%. Given the sustainability of the current demand environment, we also expect Phase 3 and Phase 4 facilities to reach high utilization levels shortly after commencing operations.

- We revise our EBITDA margin estimate higher… As the company continues to shift its product mix toward higher-margin power transformer products and its US operations demonstrate a structurally stronger margin profile, we raise our Phase 1 and 2 facilities EBITDA margin estimate from 30.5% to 32.5%.

- Updated macroeconomic assumptions… On the macro side, we have updated our 12-month USD/TRY exchange rate assumption from 50.75 to 52.70, in line with the latest CBRT Market Participants Survey results.

Share